{kind=link}

The global construction and infrastructure landscape is undergoing a profound transformation, propelled by the relentless pursuit of speed, durability, and sustainability. At the epicenter of this evolution is rapid strength concrete (RSC), a specialised category of concrete designed to attain high compressive strength within remarkably short curing periods. Its growing adoption across civil engineering, industrial architecture, and emergency repair projects underscores the significance of this material in contemporary construction.

In the forecast period, spanning from 2025 to 2035, the rapid strength concrete global market is expected to witness substantial growth. This is driven by technological innovations, escalating infrastructure investments, and evolving environmental standards.

Market Overview and Growth Projections

The market valuation for rapid strength concrete is forecasted to more than double during the decade, expanding from an estimated USD 180.5 billion in 2025 to approximately USD 396.9 billion by 2035. This depicts a robust compound annual growth rate (CAGR) of around 8.2%, reflecting its rising importance in fast-paced construction environments.

The growth of the rapid strength concrete market is driven predominantly by infrastructure upgrades, high-speed rail projects, and urban renewal initiatives. The subsequent years (2030–2035) are expected to see an acceleration with an addition of nearly USD 129.3 billion. This indicates emerging economies and develops regions adopt high-performance concrete for large-scale projects such as airports, bridges, and smart city developments.

Market Dynamics and Industry Drivers

The surge in demand for rapid-setting and early-strength concrete is fundamentally reshaped by several converging forces. Governments worldwide are channeling funds into upgrading aging infrastructure, leading to faster project completion, and minimising construction-related disruptions. The adoption of rapid strength admixtures helps in reducing construction times, allowing for expedited formwork removal, early load application, and operational commissioning. This aligns perfectly with stringent project timelines.

Additionally, the rising emphasis on sustainable construction practices is reinforcing this trend. Innovations in eco-friendly binder formulations, such as the development of low-carbon cements and chemical admixtures reduce water and cement consumption. This enables the industry to meet environmental regulations without compromising performance.

Technological advancements, including the integration of fiber reinforcement, nano-modifiers, and automation through AI-driven batching systems are enhancing the durability, workability, and consistency of rapid strength concretes. These improvements are making RSC increasingly attractive for critical infrastructure, disaster resilience, and high-performance applications.

Regional and Industry-specific Trends

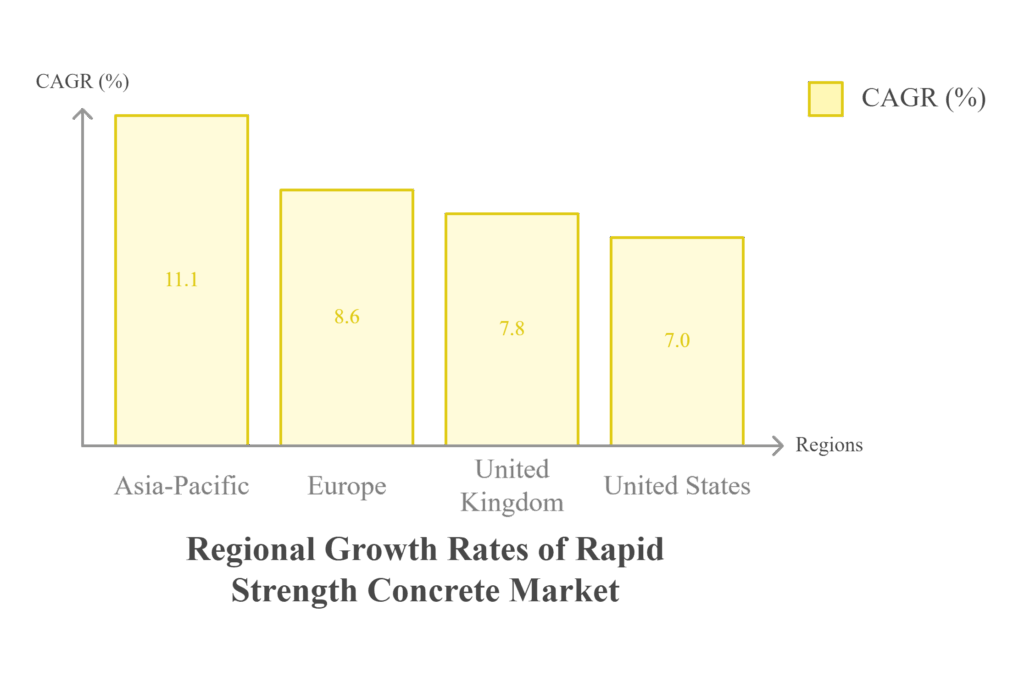

- Asia-Pacific

China leads with 11.1% CAGR driven by massive infrastructure development and high-speed railway projects. India follows a CAGR of 10.3%, supported by urban housing demand and government-backed infrastructure initiatives. The growth is driven by massive infrastructure investments as part of urbanization campaigns and initiatives like China’s Belt and Road and India’s Smart Cities Mission. Rapid strength concrete is crucial for high-rise developments, expressway expansions, and airport constructions. This minimises construction time and significant cost savings.

- Europe

The rapid strength concrete market in France is projected to expand at 8.6% CAGR. This is driven by EU sustainability directives and growing investment in public infrastructure modernisation. Use of rapid setting concrete in bridge repairs, airport runways, and emergency restoration projects ensures minimal downtime. French manufacturers integrate low-carbon cement technologies and recycled aggregates to meet stringent environmental standards. Advanced precast and 3D-printed concrete solutions gain traction in housing projects, accelerating delivery and reducing waste. Digital tools for concrete mix optimization further enhance operational efficiency.

- United Kingdom

The rapid strength concrete market in the United Kingdom is expected to grow at a CAGR of 7.8%. This is supported by infrastructure renewal programs and rising demand for accelerated construction methods. Applications in road maintenance, tunnel works, and railway station upgrades dominate the rapid strength concrete global market. Increasing adoption of automation and digital monitoring in mixing plants improves consistency and quality assurance across projects.

- United States

The rapid strength concrete market in the United States is projected to grow at 7.0% CAGR. This indicates strong adoption in rehabilitation and emergency repair projects. Aging transportation networks create demand for quick-setting concrete mixes for highways, airport runways, and bridge repairs. Federal funding for infrastructure modernisation supports large-scale use of advanced concrete technologies. The integration of fiber reinforcement and nano-modifiers improves durability and crack resistance in extreme climates.

Segmentation and Technological Insights

The market segmentation by strength, application, and region reveals intricate dynamics. The dominant strength category (40 to 80 MPa) accounts for approximately 46% of the market share, owing to its optimal balance between durability and rapid setting performance. Precast and modular construction practices also leverage rapid strength concrete for faster, safer, and more sustainable building processes. The adoption of fiber-reinforced mixes, non-corrosive admixtures, and temperature-adaptive formulations exemplifies ongoing innovation.

Challenges and Restraints

Despite promising prospects, several barriers temper accelerated growth. The high costs associated with specialized raw materials, chemical admixtures, and processing equipment pose economic constraints, especially for developing markets. Additionally, on-site mixing variability and the need for skilled labor hinder the uniform performance of rapid strength concrete, raising safety concerns.

Regulatory complexities regarding chemical use and the need to validate performance standards across regions create additional hurdles. Market players are investing in research to develop lower-cost, environmentally compliant formulations, and training programs to address these issues.

Market Forecast and Strategic Outlook

The next decade will witness a strategic shift toward sustainability, innovation, and regional market tailoring. Asia-Pacific is projected to register the highest growth, fueled by urban infrastructure expansion and government-led initiatives. North America and Europe will focus on high-end repair, upgrade, and eco-friendly formulations.

The leading companies, including BASF SE, Sika Corporation, CTS Cement, and Cemex S.A.B, are expanding R&D investments, forming strategic alliances with local manufacturers, and pioneering sustainable admixture technologies. The emergence of regional manufacturers focusing on cost-effective solutions tailored to local conditions is expected to intensify competitive dynamics.

In conclusion, the rapid strength concrete global market stands at a critical juncture where innovation, regulation, and regional development policies intertwine. Its growth trajectory is marked by a CAGR of 8.2%, reflecting the material’s vital role in shaping a resilient, sustainable, and intelligent global infrastructure ecosystem.